The Effort Exertion Error: More Effortful Saving Leads to Less Investing

Update: This work eventually turned into a published paper here. You can download it directly here.

The Idea

After meticulously saving money during my first job after college (primarily by being a daily Mint.com user), I ignored my better judgment and chose mostly conservative investment choices for my savings. This of course turned out to be a major error, as the equity market has boomed over the last decade. As a graduate student studying human psychology and consumer behavior, I knew that the best course of action going forward was not to dwell on the past - I should learn from my mistakes and just focus on the future. But whats the fun in that? Given that I had decent resources to run scientific studies on human responses to risk, I chose to instead justify my past behavior by finding empirical support for it in the general population.

So why was I conservative with my investment choices? I believe it was because I focused on how effortful it had been to accumulate savings. I had lived in the heart of high-cost Washington D.C., and saving money had required constant vigilence towards my spending, careful budgeting and expense categorizing, and a heavy dose of self-control. Because I had put forth so much effort, I believe that I grew to value my savings above and beyond what they were actually worth. Similar to the IKEA Effect where psychologists showed that people placed more value on objects that they constructed, I too found myself enamored with my savings as a thing that I didn’t want to risk losing, and lost sight of its real value - as a medium to earn more money! My aversion to losing them became heightened from the effort I had exerted, and I made investment decisions for them accordingly.

My research focused on this simple question - does exerting more effort to accumulate savings lower one’s willingness to invest those savings?

Button Pressing

To cleanly isolate effort towards savings, I came up with a simple approach - the exertion of actual, physical effort! I created a simple application that requested and tracked keyboard presses, and designed an experimental paradigm that would repeatedly ask people to press a button a certain number of times to save $1.00, and then to decide how much of that $1.00 to allocate towards an investment task. The amount of button presses required would vary from period to period ranging from very low amounts (20) to very high amounts (500). My hypothesis was that the number of button presses required - that is, the amount of effort exerted - to save the $1.00 would affect how much of the $1.00 people would be willing to allocate to an investment.

Below is an example of the button pressing procedure. Try it yourself on one of the moderate effort periods. Seriously... start pressing that "e" key!

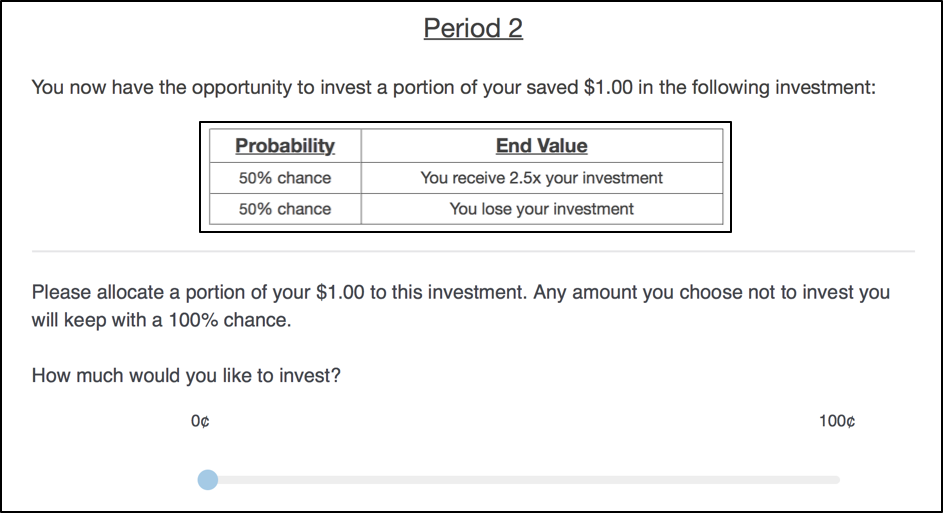

Below is an example of an investment task. Its adopted from similar investment tasks from prior literature. In my experiments, the investments always had an expected value of +25%, but the actual payoffs and probabilities differed from period-to-period.

Experimental Design

I recruited 300 people on Amazon Mechanical Turk to perform 9 periods of saving (i.e., button pressing) and investing in a 3 effort (20, 150, or 500 presses) X 3 investment type (25% chance to win 5x, 50% chance to win 2.5x,or 75% chance to win 1.66x) within-subjects design. Although every participant performed every combination of effort and investment type conditions (e.g., 20 presses/75% investment; 500 presses/25% investment, etc.), the order in which they performed these 9 periods was randomized. Participants were not informed of the outcome of each investment until the end of all 9 periods.

There was no deception in this experiment - participants in fact received $1.00 in savings for their button pushing in each period and the investment decision they made was truly simulated at the advertised probability. If the investment “won”, they received their earnings. If the investment “lost”, they lost their investment. The key independent variable was the number of button presses for a given period and the key dependent variable was how much was allocated to the investment in that period.

Results

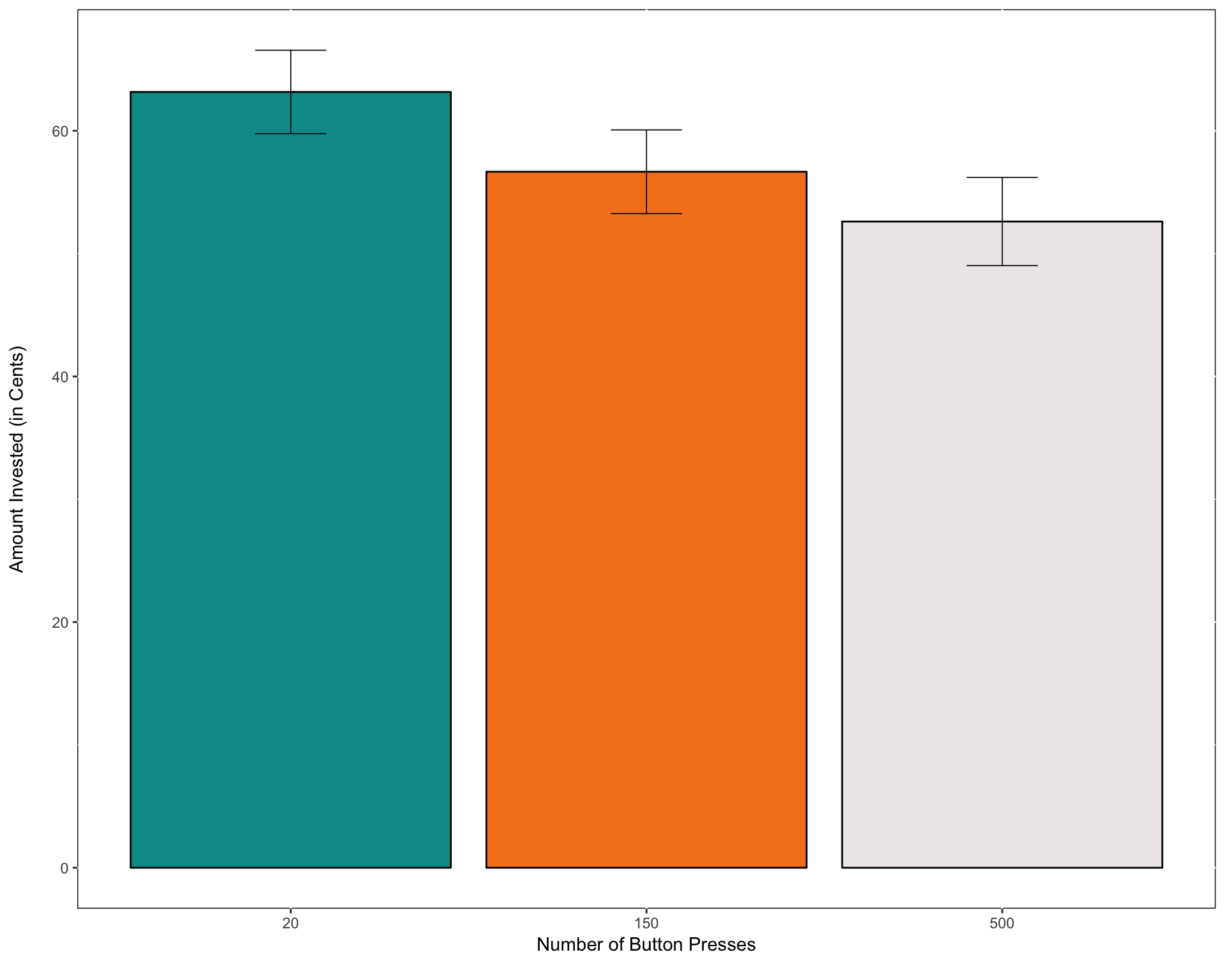

Consistent with my life hypothesis, participants allocated less of their savings to invesmtments in periods where they had exerted more effort to obtain their savings. In periods where exerted effort was low (20 presses), participants allocated an average of $0.63. In periods where exerted effort was moderate (150 presses), participants allocated an average of $0.57. In periods where exerted effort was high (500 presses), participants only allocated an average of $0.52. This was confirmed statiscally using a mixed-effects linear regression with random effects of participant (to control for variation in investment amounts between participants). These results were extremely robust - I replicated the same main effect in four additional versions of the same basic experimental paradigm. Details and results about all these studies can be seen in the paper.

Conclusion

What does this mean? Well, for starters, its quite clear that people are influenced by the effort they exert to obtain (small amounts of) money when deciding how to invest it. Does this mean that people who exert of effort to accumulate their real savings will change their true investment behaviors? Maybe - its certainly consistent with the psychology documented in my experiments - but without clear data, we can’t know for certain. A generous reader might point out that if people are getting more loss averse over extra exerted effort for such a small amount of money, perhaps when the amount of money is amplified, the loss aversion is too…

Saving and investing are both crucial behaviors for consumers. I would certainly never argue that consumers should simply exert less effort to save - if you don’t save the money, you can’t invest it! But perhaps companies and policy makers could help de-emphasize or reframe the effort that consumers incur when they save to help them invest more for their futures. Even better, perhaps saving and investing should be reframed not as two separate behaviors where one can negatively influence the other, but as one broad behavior: the accumulation of wealth.